Over the last two years, investors have treated AI as a straight-line story: more models, more tokens, more data centers, more chips, more revenues and eventually massive productivity gains. The problem is that the spending cycle has moved much faster than the cash-flow cycle. And now with full automation remaining a mirage, a correction is likely to happen. It can travel from LLM companies to hyperscalers, then to data-center builders, chip companies and eventually the fab ecosystem.

The first issue is that LLMs have been oversold. They are impressive tools, but they are not reliable full-automation systems by themselves. Hallucinations are not a small bug. They are a structural problem when companies are trying to automate legal, financial, compliance, medical or operational workflows. Gartner said more than 50% of GenAI projects were abandoned after proof of concept because of poor data quality, inadequate risk controls, rising costs or unclear business value. MIT’s 2025 GenAI Divide report also said that despite $30–40 billion of enterprise GenAI investment, 95% of organizations were getting zero return.

This is the central disconnect. A token is not enterprise software. It is not a workflow, a database, an audit trail, a compliance system or a deterministic rule engine. LLMs are powerful reasoning and generation engines, but they remain probabilistic systems. To use them safely in production, companies still need clean data, retrieval systems, guardrails, deterministic code, access controls, monitoring, exception handling and human oversight. In simple terms, AI companies have delivered powerful digital bricks, but enterprises still need architects and engineers to build safe buildings out of them.

The AI companies themselves often do not fully know what these systems can reliably do in every context. They have optimized for scale, compute, benchmarks and model capability, but enterprise value comes from solving specific workflows. A chatbot that performs well on an academic benchmark is not the same as a system that can reduce headcount, cut processing time, improve compliance and create measurable profit inside a bank, hospital, insurer or manufacturing company.

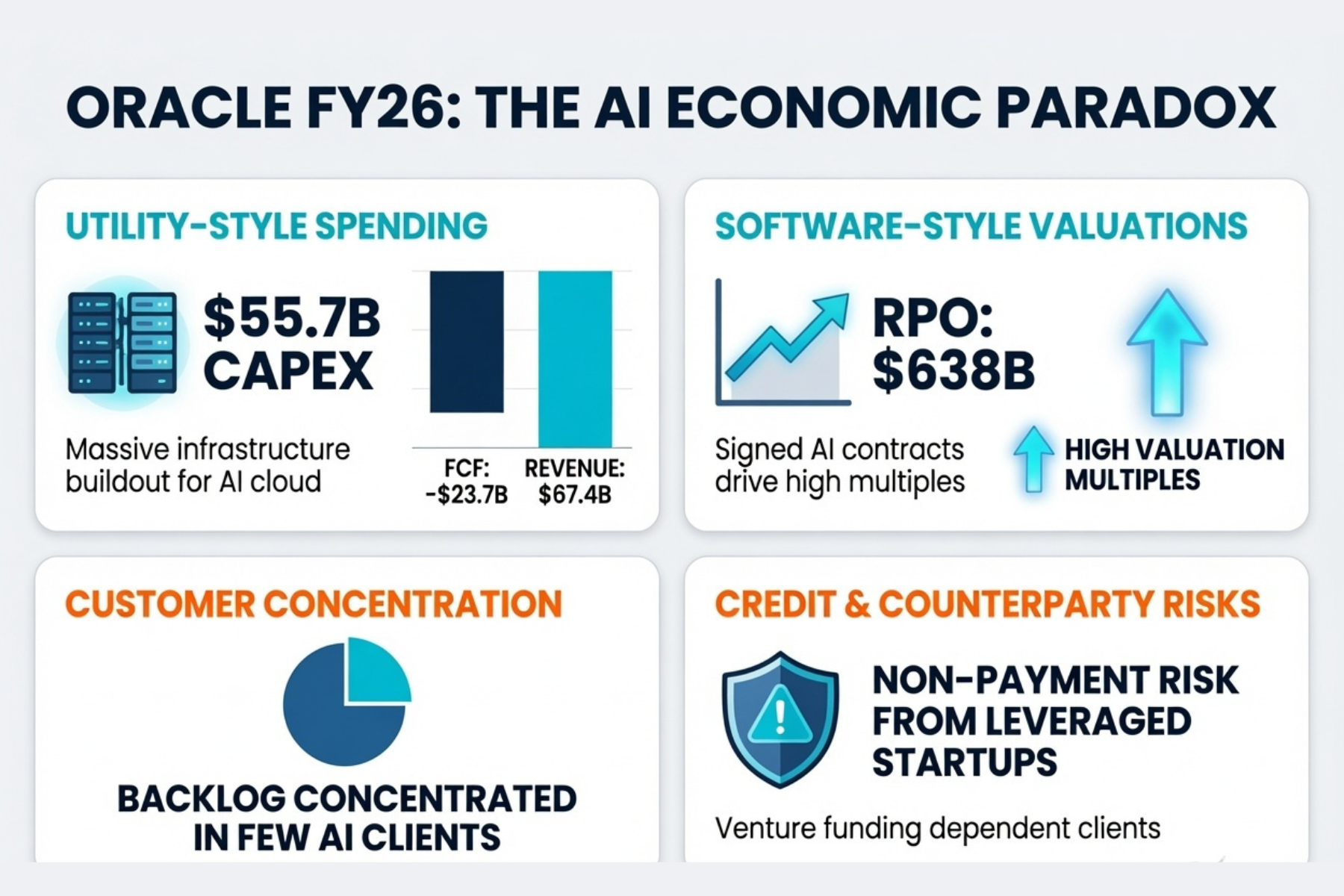

The second issue is economics. The industry is spending like a utility but is still being valued like software. Oracle is a useful example. Its FY26 revenue was $67.4 billion and its remaining performance obligations reached $638 billion, but free cash flow was negative $23.7 billion because of cloud infrastructure investment. Oracle also disclosed that its business is exposed to risks of customer non-payment and non-performance, including from some highly leveraged customers.

That matters because the AI boom is becoming a credit and capex story, not just a technology story. When a cloud company has to spend tens of billions upfront to service long-dated AI contracts, investors must ask who ultimately carries the risk if the end customer cannot monetize the compute. A signed contract is not the same as realized cash flow. Remaining performance obligations are not the same as profits.

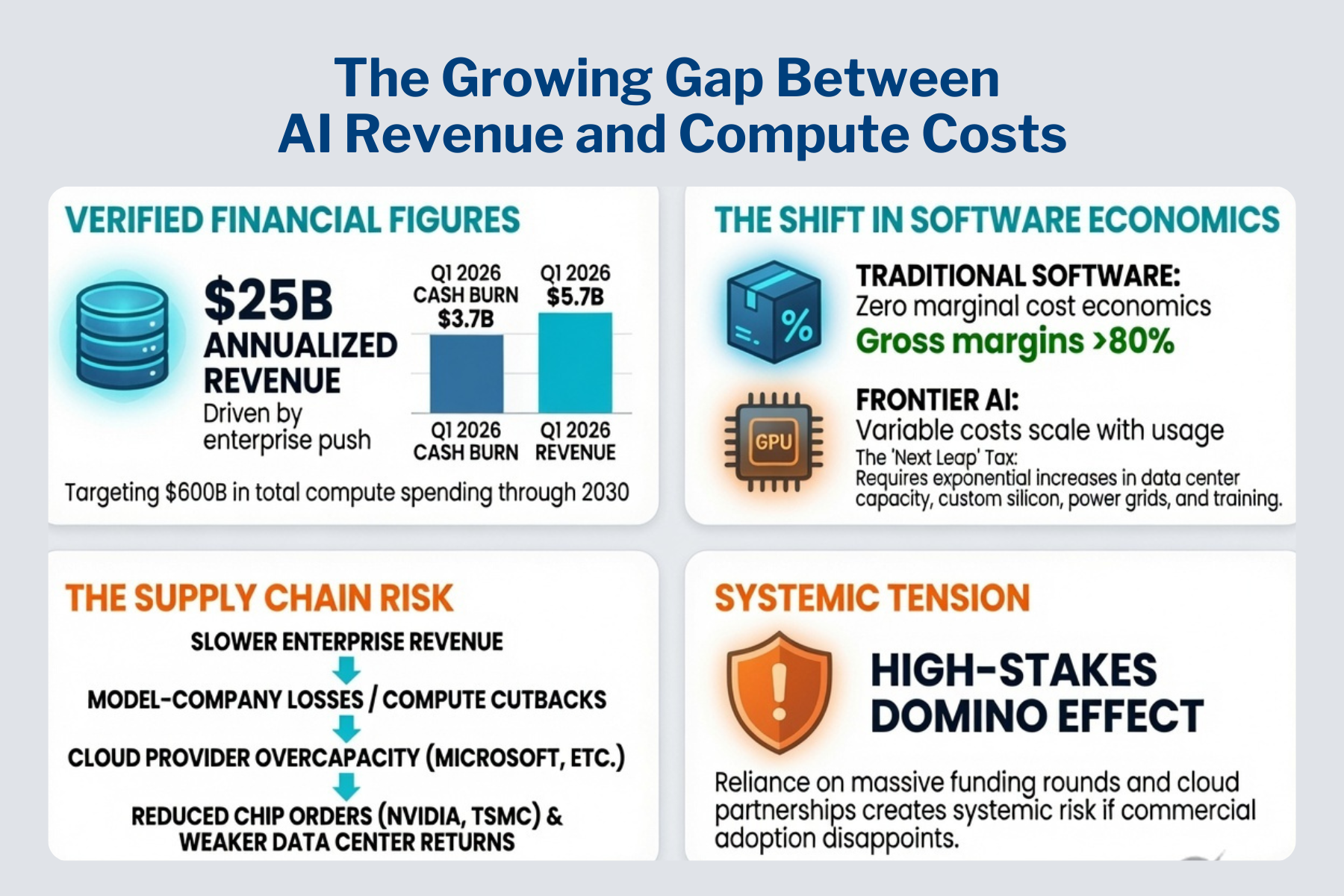

OpenAI shows the same tension from the model-company side. Reuters reported that OpenAI had crossed $25 billion in annualized revenue, but was targeting roughly $600 billion in compute spending through 2030. Reuters also reported, citing The Information, that OpenAI burned $3.7 billion in Q1 2026 on $5.7 billion of revenue.

This is not normal software economics. Traditional software scaled with very high margins once the product was built. Frontier AI is different. Every major leap needs more compute, more chips, more power and more data-center capacity. If revenue growth slows or enterprise adoption disappoints, the model-company losses can quickly become cloud-company overcapacity, which can then become lower chip orders and weaker returns on data-center investments.

There is also the issue of circularity. Nvidia announced plans to invest up to $100 billion in OpenAI while OpenAI planned to deploy Nvidia systems. Nvidia also signed a $6.3 billion agreement with CoreWeave under which Nvidia would buy unsold cloud capacity through 2032. These deals may make strategic sense for the companies involved, but they also raise an important market question: how much of AI demand is final customer demand, and how much is supplier-financed demand?

This is why the correction risk is real. If the leading AI labs and hyperscalers cannot show that AI capex is producing durable enterprise cash flows, the funding environment can change quickly. Data-center projects can be delayed. Cloud commitments can be renegotiated. AI start-ups can lose access to cheap capital. Chip demand can normalize. The market does not need AI to fail for AI stocks to correct. It only needs the profit story to arrive later than expected.

That said, AI itself is not going away. This is not a zero-value technology. AI will remain important in coding, research, analytics, customer service, document processing, software tools and internal productivity. The winners will be companies that solve specific problems and deliver measurable ROI, not those that simply sell more tokens on the promise of total automation.