To check your EPF balance, the first thing you’ll need is your Universal Account Number (UAN). This is a unique 12-digit ID assigned by the Employees’ Provident Fund Organisation (EPFO) to every contributor. What makes the UAN especially useful is that it remains the same throughout your career—even if you switch jobs. Each time you join a new employer, the EPFO simply links the new EPF account to your existing UAN, allowing you to track your entire retirement savings under a single umbrella.

1. EPFO Portal

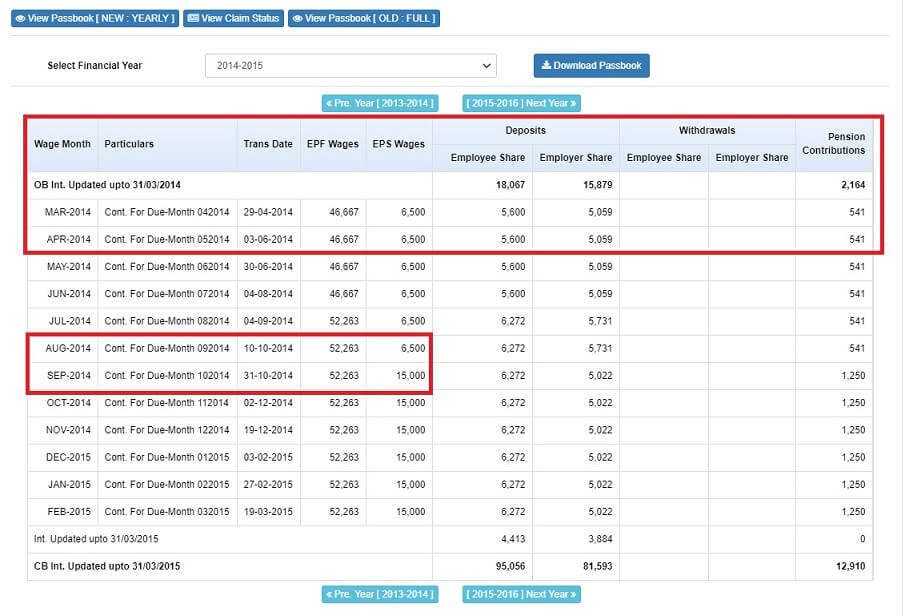

The official EPFO Member Passbook portal gives you a detailed breakdown of your EPF transactions.

Steps:

- Visit www.epfindia.gov.in

- Click on “Member Passbook”

- Log in using your UAN and password

- Select the relevant Member ID to view your passbook

Your passbook shows:

- Monthly employee/employer contributions

- EPS (pension) contributions

- Interest credited

- Withdrawals or advances

- Total balance

Ensure your UAN is activated and KYC (Aadhaar, PAN, bank) is updated to access these services.

2. UMANG Mobile App

Prefer mobile access? The UMANG app integrates EPFO services with a smooth user experience.

Steps:

- Download the UMANG app (available on Android/iOS)

- Go to: EPFO > Employee Centric Services > View Passbook

- Enter your UAN and verify via OTP

You can track balances, raise claims, and even update nominations through the app. It’s ideal for on-the-go access to your EPF.

3. SMS Service

For users without smartphone or internet access, SMS is a handy tool.

Format:

Send: EPFOHO UAN ENG

To: 7738299899

Replace “ENG” with the relevant language code (e.g., HIN for Hindi, TAM for Tamil).

Ensure:

- Your UAN is active

- Your mobile number is registered

- At least one KYC document is linked

You’ll receive an SMS with your current balance and last contribution.

4. Missed Call

Give a missed call to 9966044425 from your registered number.

Pre-requisites:

- Active UAN

- KYC (Aadhaar/PAN/bank) seeded

- Mobile number linked to UAN

You’ll get an SMS with your balance and recent contribution info.

This is the fastest, no-cost method—ideal for quick checks.

Frequency of Balance Updates

- Monthly Contributions: Employer and employee contributions are updated monthly in the passbook, usually after the 15th of the following month.

- Annual Interest: Interest is calculated monthly but credited at the end of the financial year. It usually reflects by June or July, post processing.

UAN Activation and KYC Linking: A Must for Access

Your UAN (Universal Account Number) is your lifelong EPF identifier. It stays constant across jobs and allows seamless management of multiple EPF accounts.

Why activate your UAN?

- Consolidate multiple EPF accounts

- Enable online access to passbooks and claims

- Receive real-time updates and alerts

KYC Linking Includes:

- Aadhaar

- PAN

- Bank account

Without updated KYC, you won’t be able to:

- Use SMS/missed call services

- File online claims

- Transfer accounts smoothly

Update KYC via the EPFO portal under ‘Manage > KYC’. Your employer’s HR can assist if details are pending verification.

Reading Your EPF Passbook: What to Look For

Your passbook gives a transparent view of your EPF health. It includes:

- Monthly deposits by you and your employer

- Pension (EPS) contributions

- Annual interest accruals

- Withdrawals (e.g., partial advances)

- Running balance and closing balance

Use this data to match salary deductions, plan VPF contributions, or assess liquidity options.

Smart Ways to Use Your EPF Balance in Financial Planning

Here’s how investors can integrate EPF balance checks into their strategy:

- Estimate Retirement Corpus

Project your EPF balance at retirement using calculators. Combine this with NPS, mutual funds, and other instruments to see if you’re on track. - Rebalance Your Asset Allocation

EPF is a fixed-income product. Regularly assessing its share in your portfolio helps maintain the right equity-to-debt mix. - Consider VPF to Boost Contributions

Falling short of retirement goals? Voluntarily increase your EPF contributions via VPF. It earns the same interest rate and is tax-deferred. - Plan Emergency Withdrawals Thoughtfully

EPF can be tapped for specific needs like home purchase or medical emergencies. Knowing your current balance helps assess how much liquidity is available. - Track Employer Compliance

Missed or delayed deposits can dent your long-term returns. Monthly passbook checks ensure accountability and quick resolution. - Avoid Tax Surprises on Early Withdrawals

Withdrawals before five years of continuous service may attract tax. Your passbook confirms eligibility and duration to avoid surprises. - Update Nominations Periodically

While reviewing your balance, ensure your nominee details are current. This protects your dependents from legal complications. - Include EPF in Net Worth Calculations

Your EPF corpus is a valuable part of your financial net worth. Update it during annual reviews to assess wealth accurately.