In a surprising move that caught many market watchers off guard, President Donald Trump pulled back the imposition of reciprocal tariffs on all countries except China. Conventional wisdom might suggest that a sell-off in the stock market was the trigger. However the real reason is a dramatic sell-off in US government bonds was the real catalyst—a signal too ominous to ignore.

A Timeline of Turmoil

The drama began on April 2nd when massive reciprocal tariffs were announced. In the days that followed, the US equity index, the S&P 500, plummeted by 12%, sliding from 5,670 to a low of 4,835 by April 7th. If one were to cast their gaze back to the February highs, the S&P had tumbled by over 20%. Yet amid this chaos, President Trump appeared unperturbed. The turning point, it appears, came from a very different corner of the financial world—the bond market.

Bonds: The Canaries in the Coal Mine

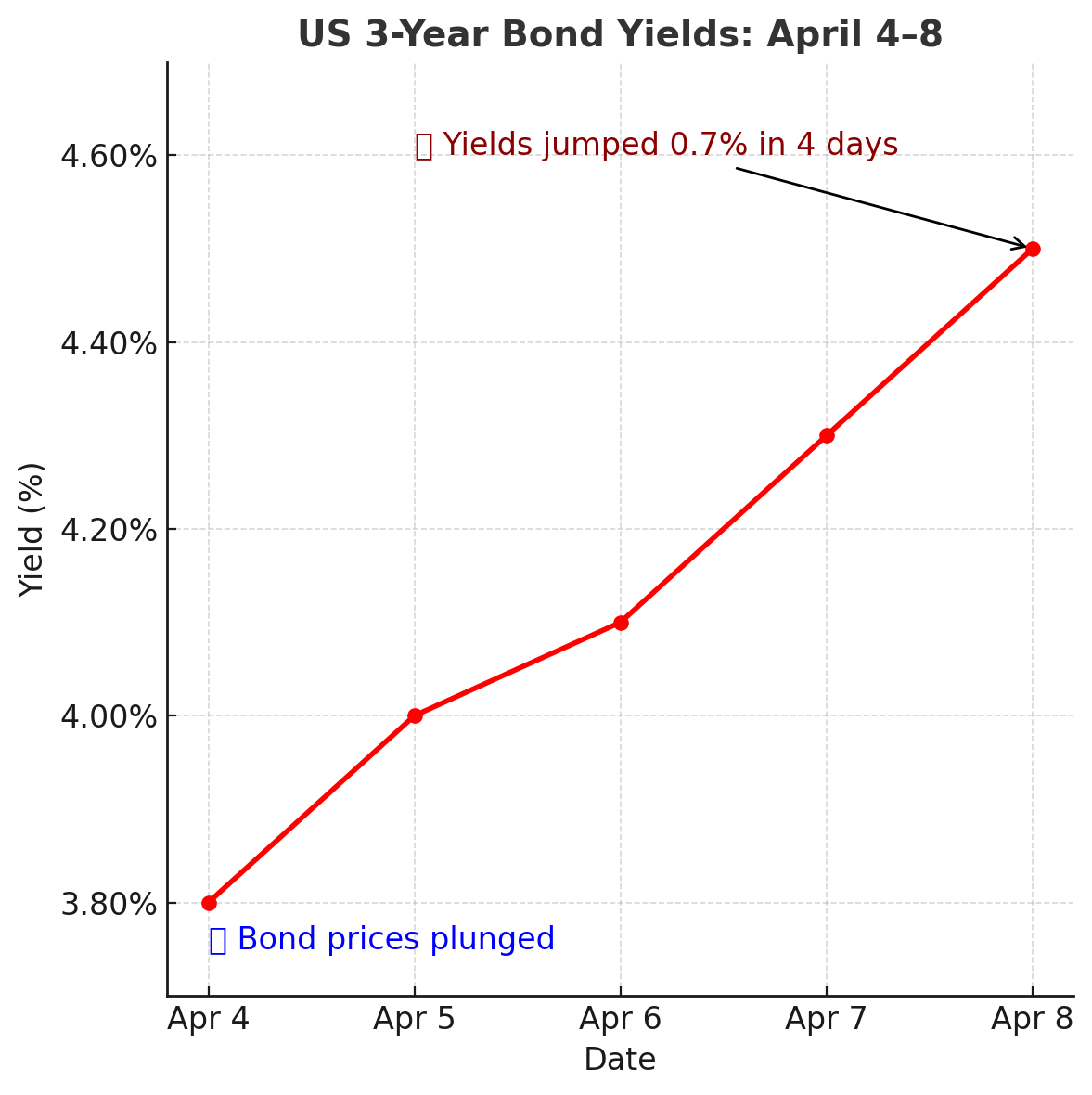

While stock markets often grab the headlines, the bond market can offer an early warning about economic shifts. Bond yields—essentially the returns investors receive from government debt—react inversely to bond prices. When bond prices fall, yields rise. On April 8th, the US government auctioned $58 billion of three-year bonds, and the results were startling. There was a dearth of buyers, leaving US banks to step in and absorb 20.7% of the offering—the highest level since December 2023. Consequently, bond yields soared from 3.8% on April 4th to a high of 4.5% on April 8th.

This rise in yields suggested that investors were suddenly less confident in buying US government debt—a worrisome development given that governments rely heavily on bond markets to finance spending beyond tax revenues.

Unpacking the Dynamics: The Role of the Basis Trade

Experts have pointed to technical trading strategies, particularly the basis trade, as a key factor. Hedge funds, often leveraging borrowed funds across various asset classes, maintain positions on both the cash and futures sides of the US bond market. When the market faced continuous declines from April 2nd to 7th, these funds faced margin calls—a stark reminder of their leveraged positions. In order to meet these calls, they were forced to liquidate their bond holdings. This unwinding of highly leveraged positions amplified the sell-off, exacerbating the decline in bond prices.

One trader recalled a similar scenario from past market dips, noting, “When you’re forced to sell in an already depressed market, the effects are magnified. It’s like a domino effect where one sale leads inexorably to another.” This anecdote is a testament to how technical factors, rather than fundamental economic indicators, can sometimes drive dramatic market moves.

Beyond the Numbers: Global Implications and Conspiracy Theories

The turmoil wasn’t confined within US borders. Governments and investors worldwide, from Japan holding over $1.08 trillion in US Treasuries to China’s $670 billion, typically regard US bonds as safe assets. Additionally, countries like India have used the accumulation of US dollars through trade surpluses to bolster their foreign exchange reserves—currently reported at $675 billion. But on April 8th, the spike in yields suggested deeper systemic issues.

Some market observers speculated that geopolitical tensions could also be at play. One line of thought suggests that big buyers—perhaps even China—may have refrained from purchasing US bonds as a subtle form of economic retaliation. There’s even speculation that major buyers like Japan, the UK, or European funds might have started offloading bonds, anticipating that rising yields would translate into higher inflation and, by extension, higher costs for corporate borrowing.

The Ripple Effects: Corporate Bonds and Market Confidence

The cascading impact of rising government bond yields soon became visible in the corporate bond sector. Since corporate bonds are typically priced at a premium over government bonds, any sudden surge in yields quickly translates into a tougher environment for companies to issue new debt. With corporate bond market activity drying up, investors began to worry about a full-blown liquidity crisis—an echo of concerns raised during the Silicon Valley Bank (SVB) crisis, where falling bond prices had sparked a broader panic.

Market veteran Treasury Secretary Scott Besant, known for his cautious approach, reportedly raised alarms about the potential fallout from a sudden crash in bond prices. The risk was clear: if banks and insurance companies found their bond portfolios suddenly devalued, they would face a liquidity crunch, potentially triggering a wave of defaults and triggering further instability across the financial system.

A Policy Reversal Rooted in Financial Prudence

Faced with these mounting concerns, corporate leaders and policy experts likely conveyed their warnings directly to President Trump. Despite earlier confidence in the tariff policy as a tool for economic management, the rapid rise in bond yields—an unmistakable marker of financial strain—forced a rethink. The decision to withdraw the tariffs (save for those against China) appears to have been a calculated move, aimed at stabilizing bond markets and averting a broader crisis.

This moment serves as a vivid reminder of how intricately connected our economic systems are. What might appear to be isolated decisions on trade and tariffs can quickly ripple through global financial markets, affecting everything from stock prices to bond yields, and ultimately, the broader economy.